Dollar-Cost Averaging (DCA) is a great approach for investments that are likely to grow over time but also likely to face volatility and bearish cycles on the way up.

If you’ve been trading digital assets (USD—BTC) for any length of time, you already know there’s no easy way to time the crypto market.

You’re likely to get in late, out early, or wait for the perfect dip and not invest at all.

This is where Dollar-cost Averaging (DCA) comes in.

Forget about timing the market —it’s time in the market that adds up.

– Warren Buffet said something along this line. A lot of variations of it have been posted since

What is Dollar-Cost Averaging?

Dollar-Cost Averaging is an investment strategy where an investor divides their total investment into smaller, often equal amounts to be invested over a specified amount of time. The scheduled purchase of assets eliminates the need to time the markets and reduces risks with one-time investments.

DCA also takes emotional buying or selling of assets off the table.

The Psychology of Investing (Crypto Edition).

Avoid bias and implement a few simple rules. Invest like the best.

How Does Dollar-Cost Averaging Work?

Dollar-cost averaging involves deciding on the total amount you wish to invest and the asset you would like to invest in. The asset could be stocks, commodities, or crypto. The strategy works for different assets and markets. Once you have made your decision, instead of investing your entire investment capital at once on the asset, you invest it in smaller equal amounts over a specific length of time.

All markets go through cycles where the prices increase or decrease over time. In crypto, this happens more often and intensely than in traditional financial markets. Seeing up to 10% movement up or down in a 24 hr period is not uncommon.

Committing to dollar-cost averaging means, you will be buying during bear markets where asset prices have dropped, and other investors are selling. You would also be buying during the times when nothing seems to be happening at all and prices are just flat. You are more likely to acquire assets at lower prices than the investors who wait for the bottom but miss it because things move fast.

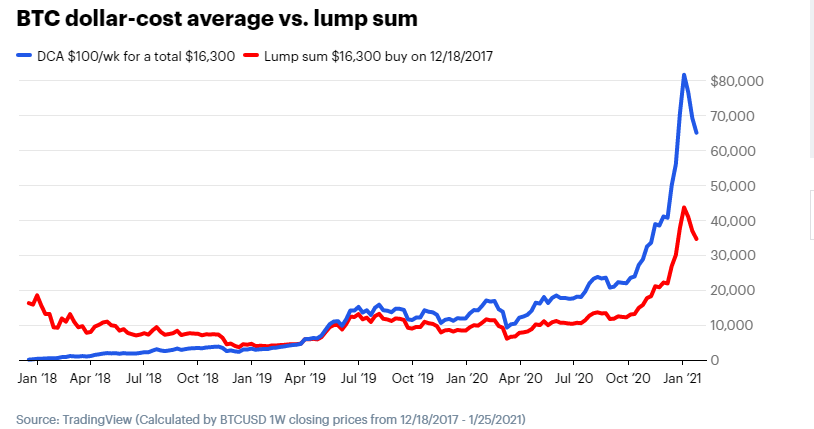

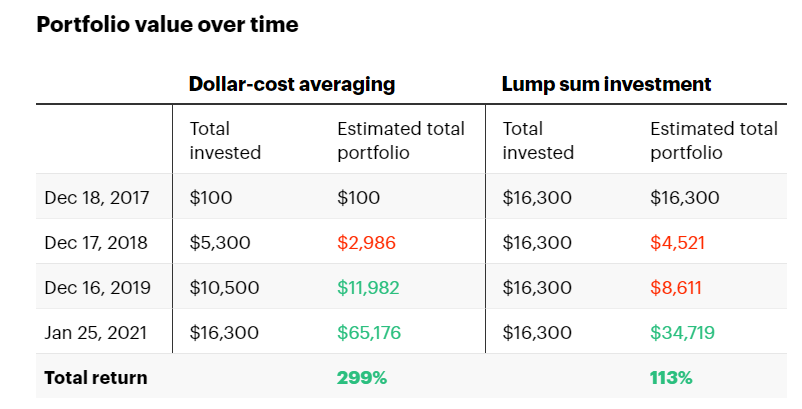

Here’s an example of buying BTC using Dollar-Cost Averaging

Let’s say you decided to invest $100 in Bitcoin every week between December 18, 2017 (near the peak) and January 25, 2021.

Using DCA, you’d have invested a total of $16,300, and your portfolio would be worth approximately $65,000.

A return on investment of 299% by January 25, 2021.

Had you decided to take that same amount ($16,300) and make a lump sum investment on December 18, 2017, the ROI during the same timeframe would have been 113%.

However, this is not always the case and depends upon the date and price you would have made your lump-sum investment. Investing a lump sum during a market downturn will create a better return, but as we said earlier, timing the market is really difficult to do, so DCA provides a better alternative for most novice to intermediate investors.

How often does DCA outperform lump-sum investing?

Often but not always.

A number of studies of DCA (investing in the stock market not crypto so take with a grain of salt) suggest that lump sum investing outperforms DCA 60 to 70% of the time. There’s less of history in crypto investing to look back at, yet investing in Bitcoin appears to mirror these results.

Cryptocurrencies are much more volatile assets than traditional stocks. Because of this, a DCA strategy works to flatten out the extreme highs and lows and sudden price movements.

As the Charles Schwab study shows, DCA usually lands you returns in the middle of the spectrum between perfect market timing and bad timing. So if you have no idea about the timing, or importantly, don’t want to stress over it. You can opt to take the middle returns and stick to a simple and consistent plan.

DCA takes the investment timing decision out of your hands so that you don’t have to worry about it or overthink it.

And most importantly of all, DCA prevents you from making bad decisions like not investing during market downturns because you’re listening to fake news and mis-information and FUD is being spread across the crypto-verse.

Not only will you sleeping peacefully, you can actually look forward to market downturns and see them as an opportunity to pick up more assets at lower cost.

Dollar-cost Averaging Out by Taking Profits

No one ever went broke by taking profits.

DCA is usually associated with buying into the market, but the principal can be used also sell out positions.

This is more often referred to as “Scaling Out” of a position or trade. Like DCA buying, Scaling Out doesn’t necessarily provide the absolute highest returns, instead it’s a worry-free way to get out of a trade or reduce a position over time.

Very few people ever buy the bottom or sell the top.

Who Should Use Dollar-Cost Averaging?

Dollar-cost averaging is ideally suited for investors who want to see success over the long term and not get too stressed out along the way.

Beginner investors:

This strategy is ideal for beginners since it’s not complicated or demanding. There is no sitting around glued to screens, reading charts, and evaluating other investment tools, waiting for what might or might not be the perfect time to sell or buy an asset.

DCA also eliminates the need to wait until you have much money to invest in an asset. This works with any amount of cash that can be spared. Investors also can implement it manually or schedule automatic purchases – if you don’t trust yourself to stick to your investment plan, choose automation.

Long-term investors:

There are generally two types of investors, long-term and short-term investors. Short-term investors don’t stay in the market for long, and they’re constantly moving assets around and chasing frequent but smaller gains. Long-term investors stay in the market for as long as they need to, and some of them may never sell.

DCA is better suited for longer-term investors. In the long-term, investment asset prices tend to rise, enabling them to take advantage of the gains that naturally happen over time.

Benefits of Dollar-Cost Averaging

Prevents bad timing: Market timing isn’t a science that many investors, even the most experienced, can perfect. Investing a lump sum at the incorrect moment can be scary and can substantially negatively impact a portfolio’s value.

Because market swings are difficult to foresee, the dollar-cost averaging technique smooths out the purchase cost, which ensures you won’t be caught receiving a low-end return on your investments.

Manage emotional investing: Emotional investing is a common occurrence, owing to a variety of circumstances such as making a large lump-sum investment and loss aversion. Emotional investing is eliminated or reduced when DCA is used.

A disciplined buying technique based on DCA allows investors to focus their efforts on their daily tasks since they are not distracted by news and information hype from different media about an asset’s short-term performance or direction.

Reduces investing stress: Trying to time the market is stressful. You need to decide what to buy and when to buy it, which just creates more work and stress.

Investments increase and decrease in price every day, sometimes to do with the investment themselves, but most often dues to news, speculation, and macroeconomic forces that push around the investment markets as a whole (e.g. interest rates, inflation rates, etc.). Staying on top of these trends is a full-time job for many, and even then, professional investors and economists tend to get it wrong quite a lot.

So if you’d like to sleep better at night, DCA can take care of the whole timing of the market issue for you and let you concentrate on what you want to buy and sell.

Are There Any Drawbacks to Dollar-Cost Averaging?

Dollar-Cost averaging has its pros, but it’s not short of cons. Some of the disadvantages that come with the investment strategy include;

Lower returns: The risk and return dynamics theory are straightforward: high risk equals high rewards, and low risk equals low returns. As a result, using a DCA strategy to decrease risk will result in slightly lower returns in the short term compared to the best-case scenario.

According to a 2012 analysis by Vanguard, a U.S.-based financial firm, a lump-sum investment would have outperformed DCA 66% of the time in the past. So history would say that most times, you’d be better off biting the bullet and investing in a lump sum when you have the money available.

Transaction fees: Since most trading platforms charge a fee for every transaction made and deposit (cash in) fees, you are likely to incur more transaction costs with dollar-cost averaging. Trading fees usually scale with the size of your trades, so even when trade fees are a percentage of the trade value, buying in a lump sum can often result in a lower percentage trade fee.

Bottom line

You’ll need discipline.

In a prolonged market correction or bear market, you will be tempted to sell — which is why, despite the common trading adage “buy low, sell high,” many people end up doing the exact opposite.

You still need to choose the right investments.

Dollar-cost averaging does not relieve you of the responsibility of deciding which assets to invest in. A lousy investment that has been dollar-cost averaged is still not a good investment.

In crypto, these are often considered the blue chips.

The best examples (2023) are probably:

BTC

ETH

ADA

LINK

MATIC

and maybe ATOM

Do Your Own Research.

Final Word

Investing in highly volatile financial markets such as cryptocurrencies can be an emotional process for beginners and experienced traders, especially when making large lump-sum investments.

The dollar-cost averaging (DCA) strategy can go a long way in minimizing anxiety around investing as you continue to systematically invest equal amounts at regular intervals, regardless of the ups and downs in the market.

Since you are building your position over time, you significantly reduce the overall impact of volatility on the price of the target asset. So over time, investments that grow will see a bigger return on investment, while investments that go down will see a lower loss.

DCA is a good way to reduce your investing stress so that you can sleep well at night.